Charging PV storage systems with grid electricity: Regulations in Germany (MiSpeL) and Austria compared

Apr 10, 2026

Anyone who wants to charge a PV storage system with grid electricity in Germany faces a regulatory framework consisting of an exclusivity option, a delimitation option, and a flat-rate option. Austria lacks a comparable regulation. This article classifies the differences and shows which rules actually apply to battery storage systems in Austria.

The question of whether a battery storage system may charge not only with PV electricity but also with grid electricity without losing the feed-in tariff has been a key regulatory issue in Germany for years. With the MiSpeL determination (market integration of storage systems and charging points), there have been clear rules since 2025 for mixed operation of green power storage and gray power storage.

In Austria, no comparable regulation exists. The reasons lie in a fundamentally different funding architecture.

Germany: MiSpeL regulates mixed operation

The exclusivity option (§19 para. 3a EEG) requires that a battery storage system may only be charged with electricity from renewable energies within a calendar year. As soon as grid electricity flows into the storage system, the entire EEG eligibility for all feed-ins of the respective year is lost. In practice, this means: no arbitrage trading, no response to market price signals, no flexible mixed operation.

The Solar Peak Act (BGBl. 2025 I No. 51, in force since February 25, 2025) introduced two new options in §19 EEG:

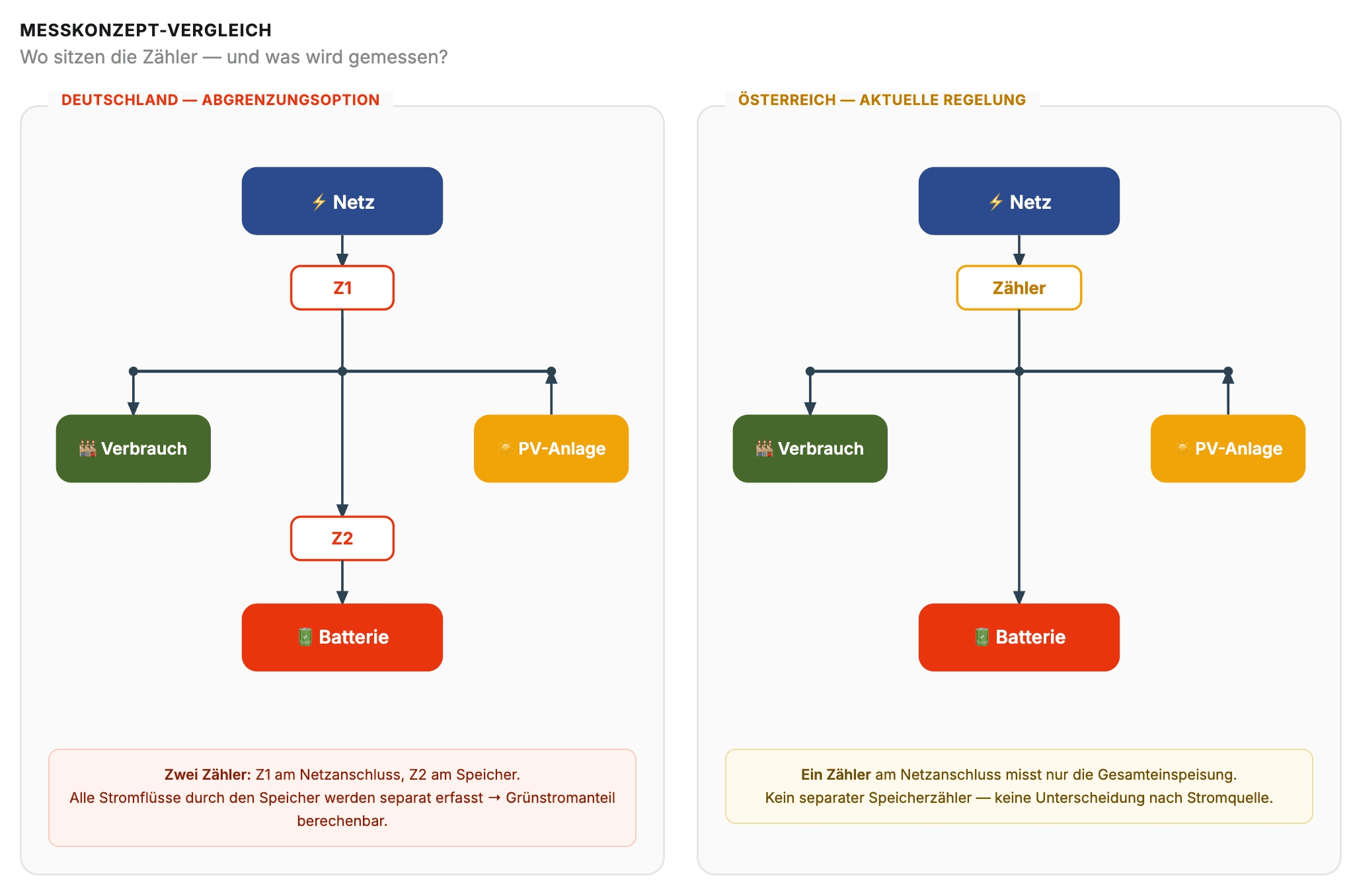

Delimitation option (§19 para. 3b): Mixed operation with PV and grid electricity is permitted. The eligible share is verified every quarter-hour via a metering concept. Two metering-instrument-compliant meters are required. Allocation follows two rules: grid electricity has priority when charging storage, storage generation has priority when feeding into the grid.

Flat-rate option (§19 para. 3c): Simplified variant for systems up to 30 kWp. Up to 500 kWh per kWp of installed PV capacity are deemed eligible on a flat-rate basis. Only one bidirectional meter is required.

In a practical article, we calculated the actual costs of the delimitation option: for a 2 MWp project, MiSpeL costs amount to €416/year — less than 1% of the feed-in tariff. We summarized the details on metering procedures and allocation rules in a separate article on the key points of MiSpeL. The BNetzA determination will be finalized by June 2026.

Austria: No exclusivity — but also no regulation

Anyone looking in Austria’s EAG (Renewable Expansion Act) for an equivalent to Germany’s exclusivity option will not find one. The market premium under §9 para. 2 EAG applies to “marketed electricity from renewable sources that is actually fed into the public electricity grid.” However, the law contains no provision concerning battery storage systems that also charge with grid electricity. The only storage-related exception in the EAG (§10 para. 1 no. 1) explicitly concerns only pumped-storage power plants.

OeMAG feed-in tariff and metering technology

The difference from Germany also lies in metering technology. In Austria, a single bidirectional smart meter at the grid connection point is used as standard. A separate generation meter behind the PV system — as is common in Germany — generally does not exist.

OeMAG remunerates based on the feed-in meter. This meter records how much electricity flows into the grid but does not distinguish whether it comes directly from the PV system or from storage. A proportional reduction of remuneration for grid electricity in storage is not provided for by law.

In practice, this means: all feed-in measured at the metering point is currently eligible for remuneration — regardless of whether the storage system was also charged with grid electricity. Anyone checking the current OeMAG feed-in tariff for 2026 will find no storage-specific restriction there.

Restrictions and open questions

Two points must be noted:

For energy communities, an exclusivity rule applies: the storage system may only be charged via the PV system and not via the grid.

The market premium is formally tied to the issuance of guarantees of origin, which are issued based on PV generation. With strongly arbitrage-oriented dispatch schedules — when measured feed-in is significantly higher than PV generation — this could become regulatorily relevant in the long term.

Battery storage funding Austria: ElWG as an economic lever

While the question of feed-in remuneration for gray power storage in Austria remains a regulatory gap, the new Electricity Industry Act (ElWG), passed on December 11, 2025, has created a more economically relevant lever.

According to §127 para. 3 ElWG, energy storage systems operated in a grid-supportive manner are exempt from demand-side grid usage and grid loss charges for 20 years. When charging the storage system from the grid — the most expensive part of operating costs — these charges are eliminated completely. For the profitability of a battery storage project, this is a larger factor than the proportional market premium.

The exact criteria for grid-supportive operation are set by E-Control via ordinance. The market consultation on this has been completed, and the new charge tariffs are to apply from January 1, 2027. For profitability calculations, it is therefore advisable to model two scenarios: with and without grid charge exemption.

In addition, the ElWG introduces for the first time a statutory definition for energy storage systems (§6 para. 1 no. 36/37), regulations on virtual metering points (§110f) for hybrid systems, and a flexibility market (§139).

In addition to grid charge exemption, operators can also apply for an investment subsidy of up to €150/kWh (max. 50 kWh) for PV-storage combinations via the EAG processing office. These investment grants are one-time and independent of later operation — whether the storage is charged with grid electricity or not does not affect the subsidy. However, PV storage funding and market premium cannot be combined.

SNAP: Lower grid charges when charging in summer

Since January 1, 2026, there has been another lever for profitability: SNAP (Summer Off-Peak Energy Price). For customers at grid level 7 (households and small businesses), the energy price component of grid charges is reduced by 20% from April 1 to September 30, between 10 a.m. and 4 p.m..

In this time window, solar power is abundant and spot prices are typically low. Anyone charging storage from the grid then benefits twice: lower spot prices and reduced grid charges. For the profitability of arbitrage models, this can be a relevant factor.

Restrictions:

Quarter-hourly measurement on the smart meter must be activated — the grid operator then applies SNAP automatically.

SNAP currently applies only to grid level 7. For commercial systems at higher grid levels, there is an optional flexibility tariff (GL 3/4), which requires an individual agreement with the grid operator.

Comparison: Germany vs. Austria

Germany | Austria | |

|---|---|---|

Regulation for storage with grid electricity | EEG §19 para. 3a–3c — regulated in detail | EAG — not addressed |

Exclusivity option | Yes, explicit (§19 para. 3a) | No (only for energy communities) |

Metering | Generation meter + feed-in meter, 15 min | Bidirectional smart meter at grid connection |

Grid charges for storage | Standard grid charges | Exempt for 20 years (ElWG §127, if grid-supportive) |

Storage support structure | Proportional market premium (ongoing, per kWh) | Investment grant up to €150/kWh (one-time) |

Double marketing prohibition | Yes (§80 EEG) | No — market premium + guarantees of origin can be combined |

Regulatory maturity | Complex, but clearly regulated | Less complex, but incomplete |

Classification for operators

Germany: The situation has been clear since MiSpeL. Mixed operation is economically almost always advantageous. The delimitation option causes low costs and enables full flexibility when charging with grid electricity.

Austria: Operators currently benefit from the absence of an exclusivity rule — mixed operation is de facto not restricted. However, this is not an explicit permission, but a regulatory gap. Operators should monitor the following points:

The E-Control ordinances on the ElWG — especially the criteria for grid-supportive operation and the grid charge exemption from 2027

The guarantee-of-origin issue for strongly arbitrage-oriented dispatch schedules

The regional differences in grid charges — in Austria these vary considerably by federal state (e.g., Burgenland +16% vs. Salzburg −9% in 2026)

The SNAP discount for systems at grid level 7

Conclusion

Germany has regulated mixed operation of PV storage systems with grid electricity for years and created a clear framework with MiSpeL. Austria has not addressed the topic in the EAG — for operators, this currently means more flexibility with less bureaucracy.

The more economically relevant lever in Austria is not the feed-in tariff anyway, but the 20-year grid charge exemption under the ElWG and the SNAP tariff. Whether Austria will introduce further regulation if battery arbitrage increases remains to be seen. Until then, it is advisable to keep an eye on E-Control’s ElWG ordinances.

Sources: