Strukturierter Stromeinkauf: Planungssicherheit und Spotpreis-Flexibilität für Industriebetriebe

Mar 9, 2026

Many industrial companies no longer obtain their electricity from the supplier at a single fixed price. Instead, experienced energy purchasers use a mix: A defined share of consumption is secured long-term at fixed prices in the futures market. The rest is procured short-term in the spot market and adapts to current market prices.

This model – often referred to in practice as structured electricity purchasing – combines the planning certainty of a fixed price with the flexibility and savings potential of the spot market. For companies with battery storage, it also significantly changes the basis of any economic simulation: electricity no longer has a uniform price but rather two different ones.

We explain how the model works, the various options available, and why a realistic battery simulation must accurately depict this tariff.

What is structured electricity purchasing?

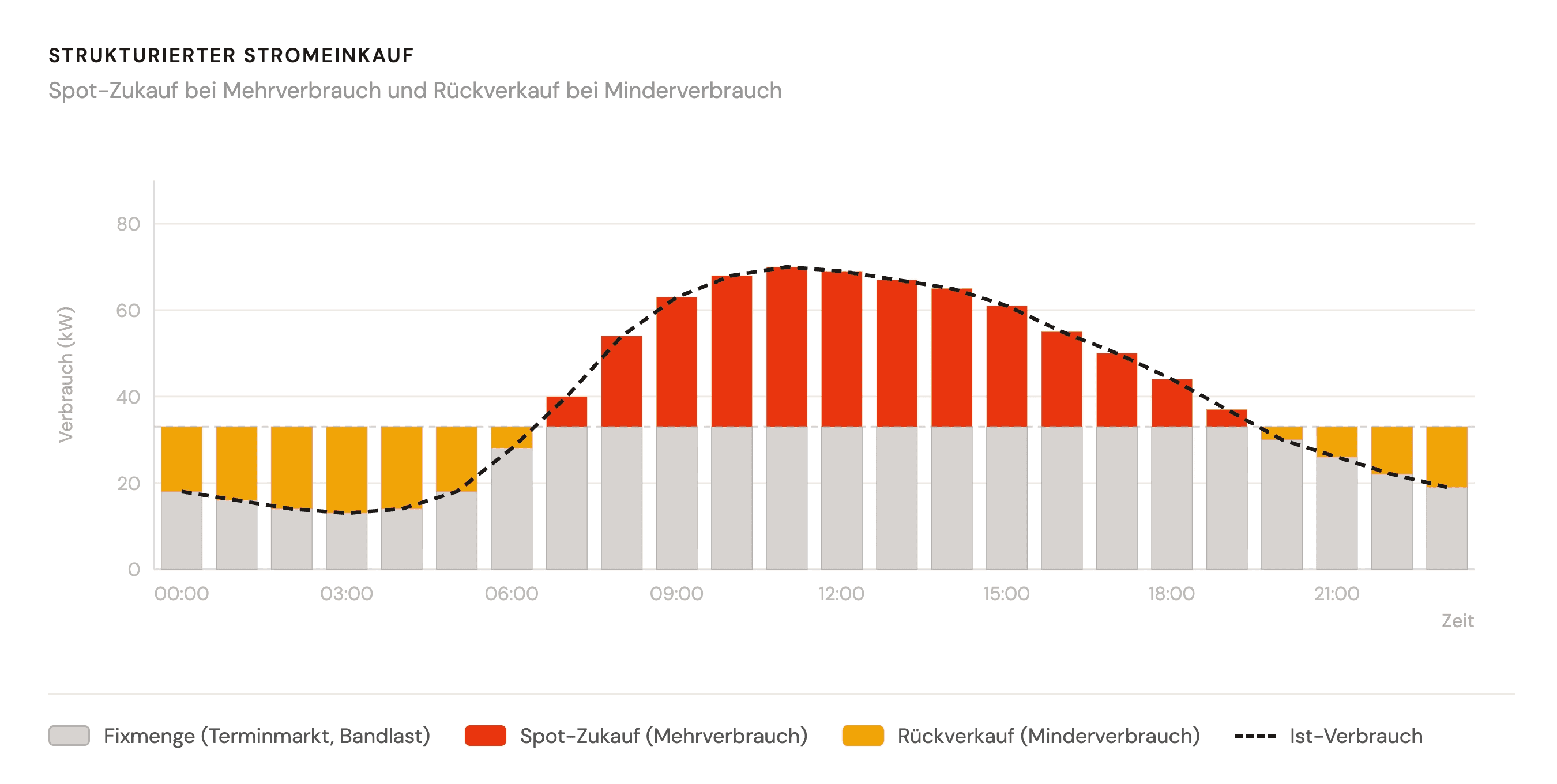

In structured electricity purchasing, the total energy demand of a company is divided into two parts: a fixed share, which is procured long-term in the futures market, and a variable share, which is purchased short-term in the spot market.

The term band purchasing is derived from the so-called band load: a constant, steady electricity load that is drawn evenly over a defined period. At the futures market of the European Energy Exchange (EEX) in Leipzig, such band deliveries can be purchased as standardized futures – typically as monthly, quarterly, or annual products with constant performance in megawatts.

The difference from the classic spot market tariff: In structured purchasing, the fixed share is priced secured, regardless of what the market does on the delivery day. Only the variable remainder is subject to daily price fluctuations.

The two common models

In practice, two fundamental variants have emerged:

Model A – Performance Threshold (classic band load)

Everything below a fixed performance threshold – for example, 700 kW – is procured in the futures market. Only the consumption that exceeds this threshold goes into the spot market. The base load is thus a truly constant "band" load: steady, every hour, regardless of the actual load profile.

Model B – Percentage Split

For instance, 80% of the forecasted annual consumption is secured fixed in the futures market, while the remaining 20% goes into the spot market. The fixed share is distributed as a constant uniform load over all hours of the year. With an annual consumption of 100,000 kWh, this means: 80,000 kWh ÷ 8,760 hours ≈ 9.13 kW constant band load – equal every hour, regardless of how much the business actually consumes during that hour. The remaining 20,000 kWh (and all deviations from the forecasted consumption) are covered via the spot market.

This model is more similar to what large industrial customers are practically using today – especially with a predictable base consumption that has seasonal and time-of-day fluctuations.

How the billing works

An important technical point: The fixation in the futures market occurs not on a quarter-hour basis. Only standardized base and peak products are tradable in the futures market – the smallest unit is a whole megawatt for a defined delivery period. Therefore, the fixation is done aggregated over months, quarters, or a year and is then spread arithmetically over all hours.

What happens in case of deviations from the plan?

Excess Consumption compared to the fixed quantity: The supplier purchases the missing quantities short-term in the spot market. The customer pays the current day-ahead price plus a surcharge for portfolio management.

Underconsumption (Over-Hedging): If more quantities are fixed than actually consumed, the supplier sells the excess energy back to the spot market. The customer receives the spot price, usually with a small discount.

There is typically no tolerance band regulation – a buffer within which smaller deviations remain uncalculated. Billing is always based on actual consumption.

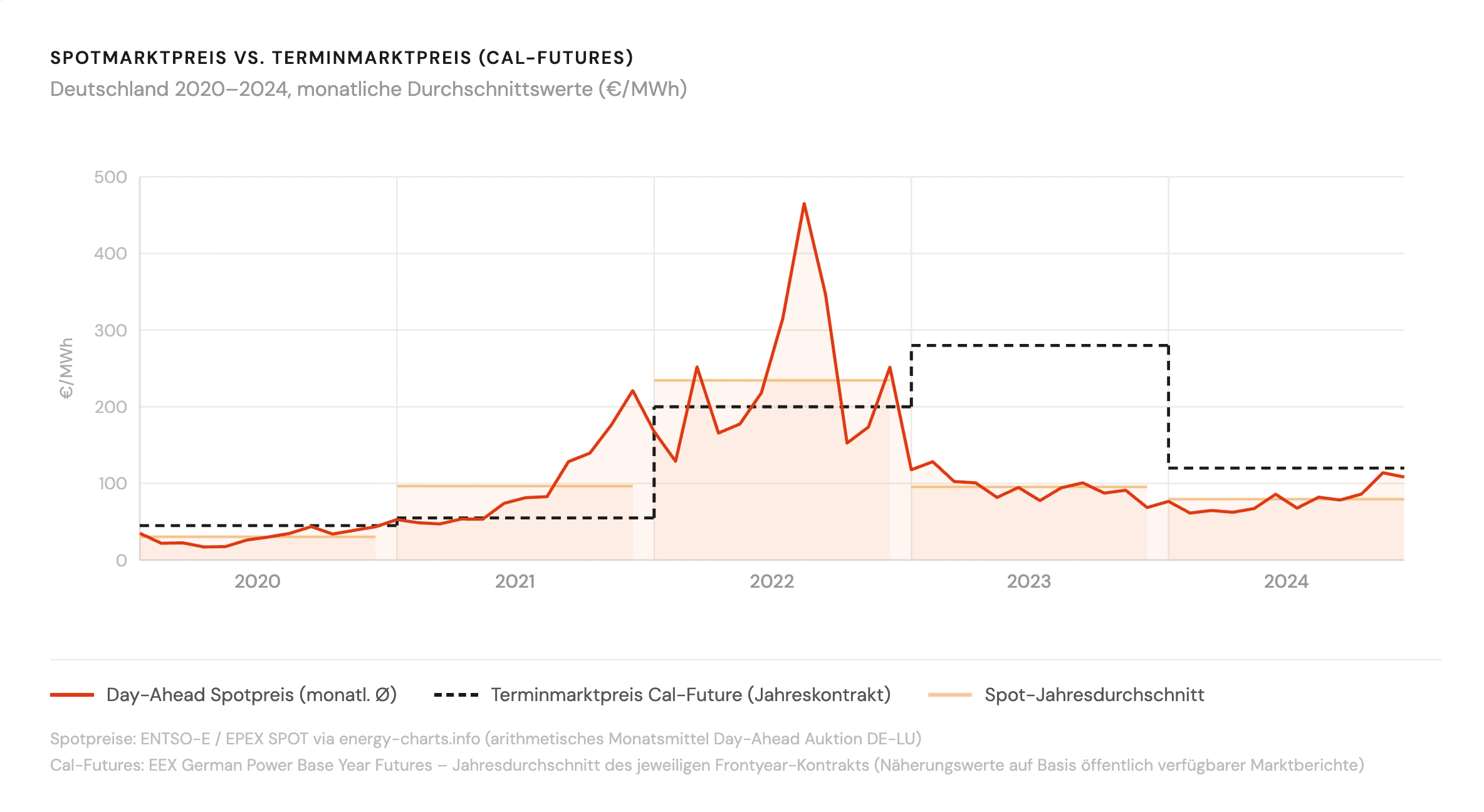

Why the futures market price includes a risk premium

Those who buy long-term in the futures market usually pay an implicit risk premium: The supplier cannot know at the time of the offer how the spot prices will develop, and prices this uncertainty. Therefore, the average spot price in the past has often been below the futures market price – a structural advantage for companies with direct spot market access.

At the same time, the spot market carries significant price fluctuations. With the expansion of renewable energies, low-price phases are occurring more frequently – for instance, on very windy or sunny days. For companies with battery storage, this opens up interesting opportunities for cost optimization.

The structured purchasing directly addresses this tension: The base load is calculably secured, while the variable share can benefit from the market.

What this means for battery storage

Those evaluating a battery storage economically typically calculate how much the storage saves through peak shaving, self-consumption optimization, or dynamic charging. These calculations directly depend on the price at which the obtained electricity is valued.

With a uniform fixed price, this is straightforward. In structured purchasing, the following applies:

The fixed price share has already been paid, regardless of how much is actually consumed. A reduction in consumption in a particular hour – because the battery is discharging – does not initially change the fixed costs. The economic leverage of the battery here lies in the variable spot price share: it can charge during low-price phases and discharge during expensive hours, thus actively optimizing the costs of the spot share.

This fundamentally changes the logic of economic calculation. Not the average price, but the marginal costs of the spot share in the respective hours are decisive for the added value of the storage. A simulation that does not take this difference into account systematically overestimates or underestimates the savings.

Lumera directly represents structured electricity purchasing in the simulation. Users can enter their fixed price share, the spot surcharge, and the procurement structure – thus receiving an economic analysis that matches their actual contract instead of relying on a simplified average price.

Who is structured electricity purchasing suitable for?

The model is especially interesting for companies with a predictable base consumption of several hundred kW and above, who either employ their own energy purchasers or work with a supplier that offers structured tariffs. Since the minimum size at the futures market is one megawatt, direct stock exchange access is only sensible for large consumers – for smaller and medium-sized companies, this is typically handled by a supplier or an energy service provider.

Those with a structured tariff appreciate the mix of budget security and market flexibility. The question is not whether, but how well the associated battery simulation represents this reality.

Conclusion

Structured electricity purchasing is not a special case for energy professionals – it is the procurement reality for many industrial large customers. Those planning a battery and working with such a tariff need a simulation that correctly models the difference between the secured fixed share and the variable spot share. Only then can an economic calculation be created that can truly be trusted.